Articles › Growth & Strategy

Growth & StrategyCan You Help Us Understand Our Unit Economics and Margins?

A fractional Finance Director helps UK SMEs decode their unit economics and margins — revealing which customers, products, and channels are truly profitable and which are not.

Understanding unit economics and margins is fundamental to running a profitable, scalable business — yet it is one of the most commonly neglected areas of financial management in UK SMEs. A fractional Finance Director makes this analysis a foundation of their engagement, because without it, every other financial decision is made in the dark.

What Are Unit Economics?

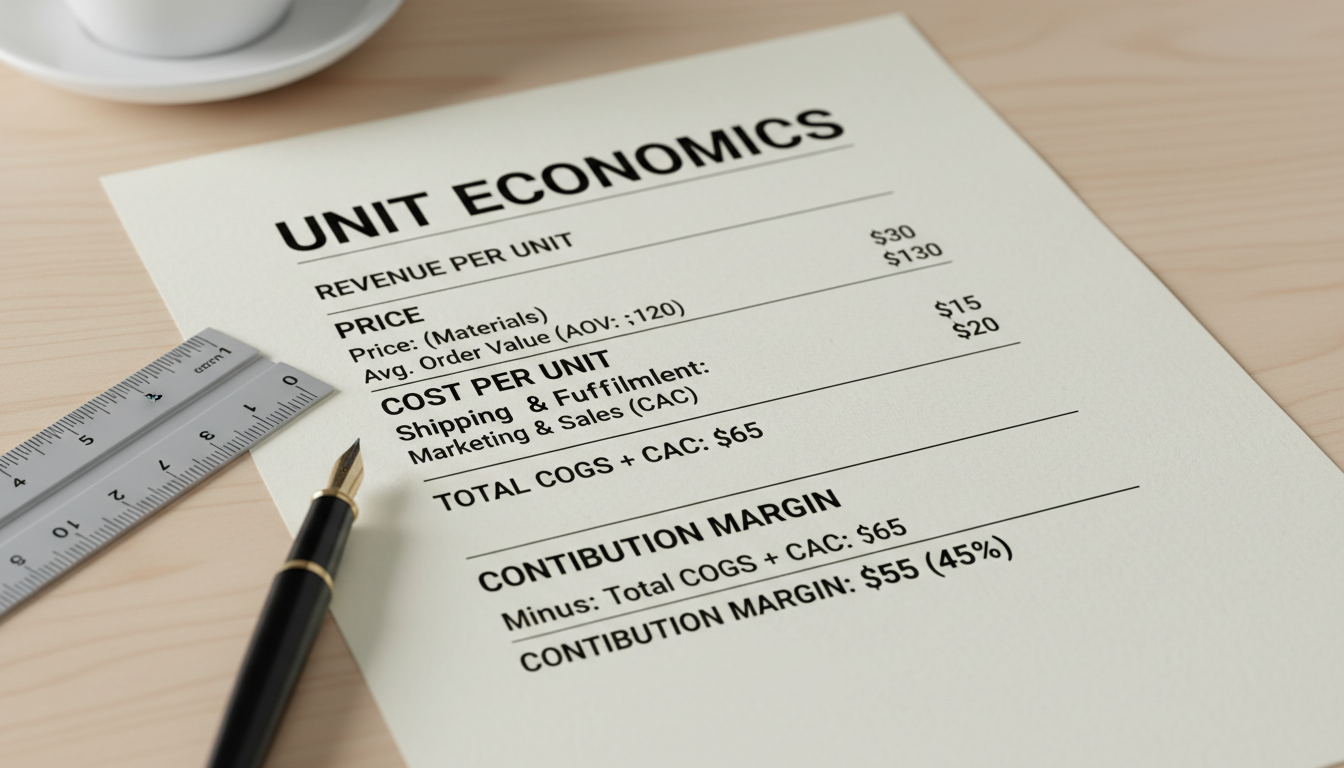

Unit economics refer to the revenues and costs attributable to a single unit of your business — typically one customer, one transaction, one product unit, or one project. They answer the question: for every unit of business we do, do we make money, how much, and is that sustainable at scale?

For a SaaS business, unit economics centre on monthly recurring revenue per customer, customer acquisition cost, and customer lifetime value. For a manufacturer, they focus on material costs, direct labour, and contribution margin per unit. For a professional services firm, they examine fee income, direct delivery cost, and profit per engagement. The framework differs by sector, but the principle is universal: you must understand the economics of your basic unit before you can scale it profitably.

The Key Unit Economics Metrics a Fractional FD Analyses

Gross Margin Per Unit

Gross margin per unit is the revenue generated by one unit minus the direct costs of producing or delivering it. This is the most fundamental unit economics metric. A fractional FD will calculate this at a granular level — by product, by service type, by customer segment, and by sales channel. The variation across these dimensions is almost always more significant than management expects.

Customer Acquisition Cost (CAC)

CAC is the total cost of acquiring a new customer, divided by the number of customers acquired in the relevant period. This includes marketing expenditure, sales staff costs, and any commissions or incentives. A fractional FD ensures that CAC is calculated on a fully-loaded basis — including the time cost of senior management involved in closing deals — rather than the narrow marketing-spend-only figure that is often reported.

Customer Lifetime Value (LTV)

LTV is the total net margin expected from a customer relationship over its lifetime. This requires an understanding of average revenue per customer, gross margin on that revenue, expected retention rates, and the time value of money. A fractional FD builds the LTV model and, critically, tracks whether actual customer behaviour matches the model's assumptions.

LTV:CAC Ratio

The ratio of LTV to CAC is the single most important unit economics metric for growth-stage businesses. A ratio below 3:1 indicates that the business is not generating sufficient return on its customer acquisition investment. A ratio above 5:1 may indicate underinvestment in growth. A fractional FD monitors this ratio continuously and investigates when it moves outside the expected range.

"Many businesses discover through unit economics analysis that they are growing themselves into unprofitability — acquiring customers below cost or serving them in ways that erode the margin they think they are making. Knowing your unit economics is not optional; it is existential."

Contribution Margin Analysis

Contribution margin — the revenue from a product or service minus all variable costs directly attributable to it — provides the clearest picture of operational profitability. A fractional FD separates fixed costs from variable costs and calculates contribution margins across the business, enabling management to understand which products and services cover their own costs and contribute to fixed overhead and profit.

This analysis is particularly powerful when combined with volume data. A product with a lower contribution margin percentage but high volume may generate more absolute profit than a product with a higher percentage margin but lower volume. The decision about which products to promote, price, or discontinue must be based on contribution margin analysis, not revenue alone.

Margin Leakage: Where Gross Margin Goes Between Invoice and Bank

Even businesses that know their headline gross margin often experience significant margin leakage — the erosion of margin between what is invoiced and what is actually retained. Common sources of margin leakage include:

- Discounts and credits not captured in margin reporting

- Returns and wastage not properly allocated to product margins

- Unbilled project overruns in professional services

- Logistics and fulfilment costs treated as overheads rather than direct costs

- Warranty and after-sales costs excluded from product profitability calculations

A fractional FD builds reporting that captures these costs properly, giving management a true picture of unit economics rather than an optimistic one.

Using Unit Economics to Drive Strategic Decisions

Understanding unit economics and margins transforms strategic decision-making. It allows management to invest in the customers, products, and channels with the strongest economics; to address or exit those that are dilutive; and to set growth targets that are grounded in the actual financial dynamics of the business rather than revenue ambitions alone.

For businesses seeking investment or preparing for a sale, demonstrable and improving unit economics are a critical component of valuation. A fractional FD ensures that your unit economics narrative is compelling, well-supported by data, and benchmarked against sector comparables.